Ford F-150 Insurance Rates

Enter your zip code below to view companies that have cheap auto insurance rates.

Michelle Robbins

Licensed Insurance Agent

Michelle Robbins has been a licensed insurance agent for over 13 years. Her career began in the real estate industry, supporting local realtors with Title Insurance. After several years, Michelle shifted to real estate home warranty insurance, where she managed a territory of over 100 miles of real estate professionals. Later, Agent Robbins obtained more licensing and experience serving families a...

Licensed Insurance Agent

UPDATED: Jun 6, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident car insurance decisions. Comparison shopping should be easy. We are not affiliated with any one car insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

If you are curious to know more about Ford F-150 insurance rates, you should know that drivers pay an average of $1,322 for full coverage, which amounts to a $110 monthly bill.

Another thing you might have asked yourself is, “How much is insurance on a Ford Raptor?” if you drive the top-end F-150 model. In order to guide you on your search for a Ford F-150 or Ford Raptor insurance policy, we’ve prepared this comprehensive article.

This guide will educate you on the differences between things such as 2019 F-150 car insurance cost, 2012 Ford F-150 car insurance costs, and 2019 Ford Raptor insurance costs.

Once you’re ready to find cheap car insurance by comparing great car insurance rates, enter your five-digit ZIP code into our free quote tool to start comparing Ford F-150 car insurance rates from top Ford F-150 car insurance companies.

Estimated auto insurance rates for a Ford F-150 are $1,298 annually for full coverage insurance. Comprehensive costs around $294, collision insurance costs $448, and liability insurance is estimated at $398. Liability-only coverage costs approximately $460 a year, and high-risk coverage costs around $2,782. 16-year-old drivers pay the most at up to $4,828 a year.

As you can see by the huge price difference (over $4,000 difference between liability-only and a teen driver with full coverage), the rate you will actually pay will most likely fall somewhere in the middle.

Car insurance coverage is generally divided into two categories, liability and physical damage coverage, with physical damage insurance consisting of comprehensive and collision. Liability insurance protects your assets if you are determined to be legally liable for damages, whereas physical damage coverage pays to fix any damage to your F-150 caused by collision, hail, fire, flood, etc.

Let’s now break down those coverages and see how they actually contribute to the cost of insurance on a Ford F-150.

Average premium for full coverage: $1,298

Premium estimates for type of coverage:

Rates are based on $500 policy deductibles, split liability limits of 30/60, and includes uninsured/under-insured motorist coverage. Rates include averaging for all 50 states and for all F-150 models.

Insurance Price Range by Risk and Coverage

As you should have noticed by now, the price of insurance can vary considerably. The illustration below gives a visual representation of the lowest and highest price scenarios, excluding the sky-high price for insuring a teen driver.

For the normal driver, insurance rates for a Ford F-150 range from as cheap as $460 for your basic liability-only policy to the much higher price of $2,782 for coverage for higher-risk drivers.

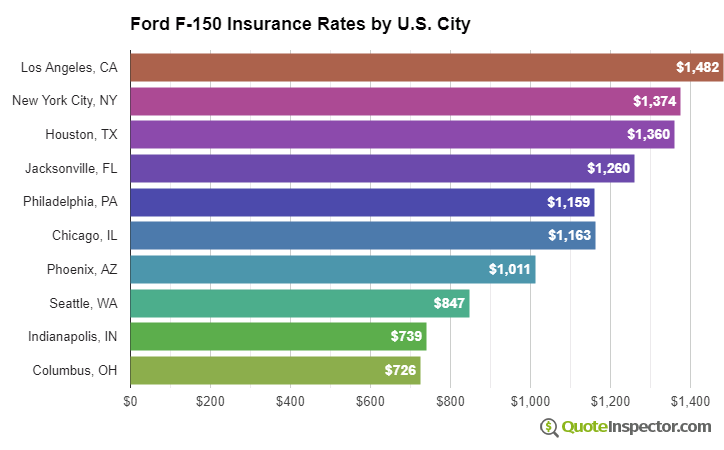

Insurance Price Range by Location

Insurance companies factor in geographic location for a number of reasons including crime rates and weather. Areas prone to higher incidents of vehicle theft or hail storms will have rates adjusted upwards to account for higher claim frequency.

Living in a larger city has a significant impact on car insurance rates. Areas with sparse population are statistically proven to have fewer physical damage claims than congested cities. The example below illustrates how geographic area affects auto insurance rates.

These rate differences illustrate why everyone should get quotes for a specific zip code and their own personal driving habits, rather than relying on rate averages.

Use the form below to get customized rates for your location.

Enter your zip code below to view companies based on your location that have cheap auto insurance rates.

More Rate Information

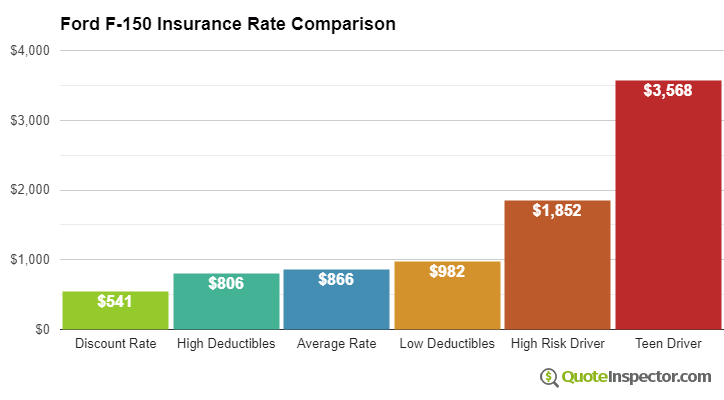

The chart below illustrates average Ford F-150 insurance rates for additional coverage choices and driver risks.

- The best full coverage rate is $762

- Choosing higher $1,000 deductibles can save about $168 each year

- The estimated rate for a 40-year-old good driver using $500 deductibles is $1,298

- Buying pricier low deductibles for comp and collision coverage will cost $1,622

- High-risk insureds with multiple tickets or accidents could pay at least $2,782

- An auto insurance policy with full coverage for a teen driver for full coverage can be $4,828 each year

Insurance prices for a Ford F-150 also have a wide range based on the model of your F-150, your risk profile, and deductibles and policy limits.

A more mature driver with a clean driving record and high physical damage deductibles could pay as little as $1,200 annually on average, or $100 per month, for full coverage. Prices are highest for drivers in their teens, where even without any violations or accidents they can expect to pay as much as $4,800 a year. View Rates by Age

If you have a few violations or you caused a few accidents, you are probably paying at least $1,500 to $2,100 extra annually, depending on your age. Ford F-150 insurance for high-risk drivers ranges anywhere from 43% to 129% more than the average rate. View High Risk Driver Rates

Opting for high physical damage deductibles can save as much as $500 each year, whereas buying more liability protection will increase prices. Switching from a 50/100 bodily injury limit to a 250/500 limit will cost up to $358 more per year. View Rates by Deductible or Liability Limit

Where you choose to live plays a big part in determining prices for Ford F-150 insurance rates. A good driver about age 40 could pay as low as $850 a year in states like Vermont, Wisconsin, and North Carolina, or at least $1,760 on average in Michigan, New York, and Florida.

| State | Premium | Compared to U.S. Avg | Percent Difference |

|---|---|---|---|

| Alabama | $1,174 | -$124 | -9.6% |

| Alaska | $998 | -$300 | -23.1% |

| Arizona | $1,078 | -$220 | -16.9% |

| Arkansas | $1,298 | -$0 | 0.0% |

| California | $1,480 | $182 | 14.0% |

| Colorado | $1,240 | -$58 | -4.5% |

| Connecticut | $1,336 | $38 | 2.9% |

| Delaware | $1,468 | $170 | 13.1% |

| Florida | $1,626 | $328 | 25.3% |

| Georgia | $1,200 | -$98 | -7.6% |

| Hawaii | $934 | -$364 | -28.0% |

| Idaho | $880 | -$418 | -32.2% |

| Illinois | $970 | -$328 | -25.3% |

| Indiana | $978 | -$320 | -24.7% |

| Iowa | $876 | -$422 | -32.5% |

| Kansas | $1,234 | -$64 | -4.9% |

| Kentucky | $1,772 | $474 | 36.5% |

| Louisiana | $1,922 | $624 | 48.1% |

| Maine | $802 | -$496 | -38.2% |

| Maryland | $1,070 | -$228 | -17.6% |

| Massachusetts | $1,040 | -$258 | -19.9% |

| Michigan | $2,256 | $958 | 73.8% |

| Minnesota | $1,086 | -$212 | -16.3% |

| Mississippi | $1,556 | $258 | 19.9% |

| Missouri | $1,154 | -$144 | -11.1% |

| Montana | $1,394 | $96 | 7.4% |

| Nebraska | $1,024 | -$274 | -21.1% |

| Nevada | $1,556 | $258 | 19.9% |

| New Hampshire | $936 | -$362 | -27.9% |

| New Jersey | $1,452 | $154 | 11.9% |

| New Mexico | $1,150 | -$148 | -11.4% |

| New York | $1,370 | $72 | 5.5% |

| North Carolina | $750 | -$548 | -42.2% |

| North Dakota | $1,062 | -$236 | -18.2% |

| Ohio | $896 | -$402 | -31.0% |

| Oklahoma | $1,336 | $38 | 2.9% |

| Oregon | $1,190 | -$108 | -8.3% |

| Pennsylvania | $1,238 | -$60 | -4.6% |

| Rhode Island | $1,732 | $434 | 33.4% |

| South Carolina | $1,178 | -$120 | -9.2% |

| South Dakota | $1,096 | -$202 | -15.6% |

| Tennessee | $1,138 | -$160 | -12.3% |

| Texas | $1,566 | $268 | 20.6% |

| Utah | $962 | -$336 | -25.9% |

| Vermont | $890 | -$408 | -31.4% |

| Virginia | $776 | -$522 | -40.2% |

| Washington | $1,006 | -$292 | -22.5% |

| West Virginia | $1,190 | -$108 | -8.3% |

| Wisconsin | $900 | -$398 | -30.7% |

| Wyoming | $1,156 | -$142 | -10.9% |

Insurance Rates by Trim Level and Model Year

Rates assume 2023 model year, a 40-year-old male driver with no accidents or violations, $500 comprehensive and collision deductibles, minimum liability limits, and uninsured/under-insured motorist coverage included. Rates are for comparison only and are averaged for all 50 U.S. states.

| Model Year | Comprehensive | Collision | Liability | Total Premium |

|---|---|---|---|---|

| 2024 Ford F-150 | $306 | $452 | $390 | $1,306 |

| 2023 Ford F-150 | $294 | $448 | $398 | $1,298 |

| 2022 Ford F-150 | $284 | $436 | $416 | $1,294 |

| 2021 Ford F-150 | $274 | $418 | $430 | $1,280 |

| 2020 Ford F-150 | $260 | $404 | $442 | $1,264 |

| 2019 Ford F-150 | $250 | $374 | $452 | $1,234 |

| 2018 Ford F-150 | $240 | $352 | $456 | $1,206 |

| 2017 Ford F-150 | $230 | $316 | $460 | $1,164 |

| 2016 Ford F-150 | $214 | $292 | $460 | $1,124 |

| 2015 Ford F-150 | $206 | $272 | $464 | $1,100 |

| 2014 Ford F-150 | $202 | $254 | $474 | $1,088 |

| 2013 Ford F-150 | $186 | $236 | $474 | $1,054 |

| 2011 Ford F-150 | $170 | $196 | $474 | $998 |

| 2008 Ford F-150 | $152 | $156 | $460 | $926 |

| 2007 Ford F-150 | $150 | $150 | $452 | $910 |

| 2006 Ford F-150 | $138 | $142 | $446 | $884 |

| 2005 Ford F-150 | $132 | $134 | $442 | $866 |

Rates are averaged for all Ford F-150 models and trim levels. Rates assume a 40-year-old male driver, full coverage with $500 deductibles, and a clean driving record.

How to Buy the Best Cheap Ford F-150 Insurance

Finding better rates on Ford F-150 insurance takes being a good driver, having a good credit history, paying for small claims out-of-pocket, and dropping full coverage on older vehicles. Invest the time to compare rates at least once a year by getting quotes from direct insurance companies, and also from several local insurance agents.

The following list is a quick review of the primary concepts that were presented in the illustrations above.

- It is possible to save up to $150 per year just by quoting online well ahead of the renewal date

- High-risk drivers with a DUI or reckless driving violation pay on average $1,480 more every year than a safer driver

- Increasing policy deductibles could save up to $500 each year

- Drivers age 16 to 20 pay higher prices, with premiums being up to $402 per month including comprehensive and collision insurance

Now that’s a lot of information to absorb from one article. The key takeaways we want you to learn are that auto insurance costs are constantly changing. The cost to insure a Ford F-150 today will be different that the cost in six or 12 months.

Insurance companies adjust rates frequently as their underwriting goals and profitability outlook changes. A downturn in the investment markets can result in an uptick in car insurance rates as insurance companies try to maintain profitability and appease their shareholders.

If it feels like you’re cutting checks at the whim of a big corporation, you’re right, but you do actually have considerable control over how much you pay for auto insurance. Personal risk factors play the largest part in determining the cost to insure a Ford truck, so take the following things into consideration the next time you hit the highway.

- Avoiding tickets and at-fault accidents are the best way to keep rates down.

- Keep an eye on your credit score and take proactive steps to ensure it remains at a high level. 720 and above is generally considered good, with anything over 800 being excellent.

- Shop around because there are many, many options for auto insurance and you are not obligated to remain with the same company.

- The younger you are, the more expensive it will be to buy car insurance. You can raise your deductibles to lower the cost, but just make sure you have enough savings to cover the extra out-of-pocket expense you may incur if you have a physical damage claim.

- Check with your agent or company to make sure you’re getting every discount you’re entitled to. Some discounts, like being a member of a professional organization, are not always clearly stated so make sure your agent or company reviews every possible discount available.

Finding the best insurance for your Ford F-150 is a balance of cost and company reliability. If you just want the cheapest insurance, it’s an easy comparison on price alone. But if you want a company that has a good price along with a stellar reputation, then you will need to do a little more work.

Online reviews are a great place to start to narrow down your options, and also talk to friends and family about their experiences with their insurance company. You can quickly create a small list of candidates to obtain price quotes from and you’ll be well on your way to finding the best insurance for America’s best-selling truck, the Ford F-150!

As you can see from the information we’ve gone over to this point, there are several moving parts that ultimately determine Ford F-150 costs. Take advantage of our free online quote tool below to start comparing Ford F-150 rates from several companies.

Compare Quotes From Top Companies and SaveFree Car Insurance Comparison

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

What are the safety ratings of the Ford F-150?

When quoting a driver, insurance companies will look at the safety features and ratings of the model you drive in order to determine the risk of injury to you as well as the risk of damage to your Ford F-150. Based on that, you can have an idea of potential future the Ford F-150 maintenance cost.

Take a look at the following safety ratings of the Ford F-150 as determined by the Insurance Institute for Highway Safety (IIHS).

- Small overlap front (driver-side): Good

- Small overlap front (passenger-side): Good

- Moderate overlap front: Good

- Side: Good

- Roof strength: Good

- Head restraints and seats: Good

As you can see from these crash test results, the Ford F-150 received the highest mark possible in all six categories.

Ford F-150 Compared Against Other Vehicles in the Same Class

The Insurance Institute for Highway Safety classifies the Ford F-150 as a large pickup truck.

If you are curious to know how the Ford F-150 stacks up to other similar models, take a look at the following three models. Each page provides information on the insurance rates for each comparable pickup so you can cross-reference them with the Ford F-150.

Now that we have gone into great detail about Ford F-150 insurance costs, is there anything you want to know more about? If not, be sure to use our free online tool to start comparing Ford F-150 car insurance quotes from top auto insurance companies today.

Rate Tables and Charts

Rates by Driver Age

| Driver Age | Premium |

|---|---|

| 16 | $4,828 |

| 20 | $2,960 |

| 30 | $1,352 |

| 40 | $1,298 |

| 50 | $1,186 |

| 60 | $1,162 |

Full coverage, $500 deductibles

Rates by Deductible

| Deductible | Premium |

|---|---|

| $100 | $1,622 |

| $250 | $1,472 |

| $500 | $1,298 |

| $1,000 | $1,130 |

Full coverage, driver age 40

Rates by Liability Limit

| Liability Limit | Premium |

|---|---|

| 30/60 | $1,298 |

| 50/100 | $1,546 |

| 100/300 | $1,645 |

| 250/500 | $1,904 |

| 100 CSL | $1,585 |

| 300 CSL | $1,804 |

| 500 CSL | $1,964 |

Full coverage, driver age 40

Rates for High Risk Drivers

| Age | Premium |

|---|---|

| 16 | $6,866 |

| 20 | $4,698 |

| 30 | $2,840 |

| 40 | $2,782 |

| 50 | $2,654 |

| 60 | $2,630 |

Full coverage, $500 deductibles, two speeding tickets, and one at-fault accident

If a financial responsibility filing is required, the additional charge below may also apply.

Potential Rate Discounts

If you qualify for discounts, you may save the amounts shown below.

| Discount | Savings |

|---|---|

| Multi-policy | $68 |

| Multi-vehicle | $66 |

| Homeowner | $19 |

| 5-yr Accident Free | $91 |

| 5-yr Claim Free | $82 |

| Paid in Full/EFT | $57 |

| Advance Quote | $62 |

| Online Quote | $91 |

| Total Discounts | $536 |

Discounts are estimated and may not be available from every company or in every state.

Compare Rates and Save

Find companies with the cheapest rates in your area